VA Loan vs Conventional Loan

Choosing

the right mortgage is a major financial decision.

For those who have served in the military, the choice often comes

down to a VA loan vs. a conventional option. Both can help you understand the difference between VA loans and conventional loans. buy a home, but they work in very different ways.

TheDepartment

of Veterans Affairs backs VA home loans, while no

government agency backs conventional financing. Understanding the key

differences is essential to saving money and finding the right fit

for your family.

Choosing

the right mortgage is a major financial decision.

For those who have served in the military, the choice often comes

down to a VA loan vs. a conventional option. Both can help you understand the difference between VA loans and conventional loans. buy a home, but they work in very different ways.

TheDepartment

of Veterans Affairs backs VA home loans, while no

government agency backs conventional financing. Understanding the key

differences is essential to saving money and finding the right fit

for your family.

This guide breaks down the loan requirements, costs, and benefits of each option. We will examine VA loans and conventional mortgages side by side. Whether you are a first-time buyer or a veteran investor, knowing the specifics of each type of loan will help you make a smart choice. Let's explore the details of a VA loan and a conventional mortgage to see which one matches your financial goals.

What is a VA Loan?

A VA loan is a benefit for active-duty service members, veterans, and eligible surviving spouses. Private lenders, such as banks and mortgage companies, provide these loans. The Department of Veterans Affairs guarantees a portion of the loan to the lender. This guarantee protects the lender if the borrower defaults, making VA loans a safer option in comparison to conventional loans. Because of this backing, lenders can offer special terms to those who qualify for VA benefits.

These loans are intended to make home buying more accessible for those who served. They remove many of the common barriers to getting financing. For example, VA loans typically do not require a down payment. They also have flexible credit guidelines. This benefit is an effective tool, but it does come with specific rules, such as the VA funding fee and the requirement that the home be your primary residence.

Key Benefits of a VA Loan

The advantages of a VA loan are significant and may result in significant savings over the years. These benefits make the VA program, compared with conventional loans, an important consideration for borrowers and one of the best options for military members.

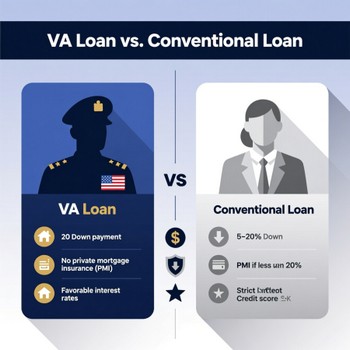

- No Down Payment: You can finance 100% of the home's purchase price. This is the biggest advantage for many buyers who haven't saved a large down payment.

- No Private Mortgage Insurance (PMI): Unlike other loans, these options do not require PMI. This saves you hundreds of dollars each month.

- Competitive Interest Rates: Because the government backs the loan, lenders often offer lower interest rates in comparison to conventional mortgages.

- Easier Credit Qualifications: The VA does not set a minimum credit score. While lenders can have their own rules, they are often more flexible with credit history.

- Limited Fees: VA loans typically have lower closing costs in comparison to conventional loans. The VA limits the types of costs lenders can charge. Sellers can also pay up to 4% of the home's price in concessions to help with your expenses.

What is a Conventional Loan?

A conventional loan is a mortgage that is not insured or guaranteed by the federal government. It is the most common financing option in the United States. Most conventional mortgages are available through banks, credit unions, and online lenders. They often follow guidelines set by Fannie Mae and Freddie Mac, which are government-sponsored enterprises. These are called "conforming" loans.

Because the government does not back them, the lender takes on more risk. To offset this, conventional options require stricter standards for borrowers. You typically need a higher credit score and a larger down payment compared to government-backed options such as VA or FHA. However, they offer great flexibility in terms of property types. You can use conventional financing to buy a primary residence or a second home, or to finance an investment property.

Key Features of a Conventional Loan

Conventional mortgages are available to a wide range of borrowers, not just those with military service. Their features appeal to buyers with strong financial profiles.

- Low Down Payment Options: You can put down as little as 3% for first-time homebuyers or 5% for repeat buyers. This makes them accessible, though you will have to pay PMI on a conventional loan, unlike VA loans, which do not require it.

- Private Mortgage Insurance (PMI): If your down payment is less than 20%, you must pay PMI. This protects the lender. A key advantage is that you can cancel PMI once you have 20% equity in your home.

- Flexible Property Types: You can use this option for a vacation home, a rental property, or a second residence. This is a major difference from VA loans.

- Higher Loan Limits: Conforming loan limits are high, allowing you to borrow more for expensive homes. For homes above that limit, you can get a jumbo loan.

- Speed and Certainty: Because they are not government-backed, conventional loans require a more thorough approval and closing process.

VA Loan vs. Conventional: The Main Differences

When weighing your options, the decision depends on your eligibility, finances, and home-buying goals. The table below illustrates the core differences to help you understand both sides.

| Feature | VA Loan | Conventional Loan |

|---|---|---|

| Down Payment | $0 required. You can finance the entire purchase price. | 3% to 20% required. At least 3% down, but 20% is needed to avoid PMI. |

| Mortgage Insurance | None. No monthly insurance premiums. | PMI is required if the down payment is less than 20%. Cancelable when you reach 20% equity. |

| Credit Score | No VA minimum. Most lenders prefer a credit score of 620 or higher, but there is flexibility. | 620 is the standard minimum. Better rates require a score of 740 or higher. |

| Interest Rates | Typically lower. Government backing allows lenders to offer very competitive rates. | Rates vary by credit. Borrowers with excellent credit can get rates comparable to those available through the VA. |

| Property Type | Primary residence only. You must live in the home - no second home or investment properties. | Any property type. Primary residences, vacation homes, and investment properties are all eligible. |

| Funding Fee | VA funding fee required (unless exempt). This one-time cost ranges from 1.4% to 3.6% of the loan amount. | No funding fee. However, you will pay for closing expenses and possibly PMI. |

| Loan Limits | No limits This option is notably helpful for borrowers with full entitlement who qualify for a VA loan. You can borrow as much as you qualify for. | Conforming loan limits apply (e.g., $806,500 in 2025 for most areas). Higher limits exist for jumbo loans. |

This comparison shows that the differences are stark. VA loans are built for accessibility and low upfront costs. Conventional mortgages reward strong credit and a larger down payment with long-term flexibility.

Is a VA Loan Better Than a Conventional Option?

Deciding which option suits your needs depends on your personal situation. For many eligible veterans, VA loans win compared with conventional loans due to their favorable terms. The ability to buy a home with no money down and no PMI is hard to beat. It frees up cash for other expenses, like moving or renovations. Lower interest rates also mean a lower monthly payment than conventional financing with the same terms. If you have a limited budget for a down payment or have a lower credit score, this option is likely the better choice.

However, there are times when conventional financing may be a smarter financial move. If you have excellent credit and can make a 20% down payment, you can avoid both PMI and the VA funding fee. This could result in lower overall costs, especially if you plan to stay in the home for a long time. Also, if you are looking to buy a vacation home or an investment property, conventional financing is your only option, as VA loans require owner-occupancy.

Cost Analysis: Funding Fee vs. Mortgage Insurance

One of the biggest financial differences between these two products is how you pay for the lender's risk. With a VA loan, you pay the VA funding fee. This is a one-time cost that assists in offsetting the program's cost to taxpayers. The amount depends on your down payment and whether it's your first time using the benefit. For first-time users with no money down, the fee is 2.15% of the loan amount. You can roll this fee into your loan so you don't have to pay it out of pocket at closing. Veterans receiving disability compensation are exempt from this fee.

With conventional financing, you pay for PMI if your down payment is under 20%. This monthly premium is added to your mortgage payment. The cost varies but usually ranges from 0.5% to 1.5% of the original loan amount per year. For a $300,000 loan, that could be an extra $125 to $375 per month. Unlike the one-time VA funding fee, you pay PMI every month until you build up 20% equity in your home and request its removal. Over several years, these payments can add up significantly.

Credit and Qualification Standards

The loan requirements for credit and income differ greatly between these two products. For conventional financing, lenders stick fairly closely to Fannie Mae and Freddie Mac guidelines. You generally need a credit score of at least 620. Your debt-to-income ratio (DTI) - which compares your monthly debt payments to your income - should typically be below 45% or 50%. A stable job history and sufficient income to cover the new payment are also required.

VA loans offer more leeway. The VA does not set a minimum credit score, allowing lenders to be more flexible with applicants who have past credit issues. After a major financial event such as bankruptcy or foreclosure, the waiting period to qualify is often shorter than that for conventional options. The VA also looks at "residual income" - the money you have left after paying major expenses - rather than relying solely on a strict DTI ratio. This all-encompassing view can help veterans qualify even if their DTI is slightly higher than conventional standards allow.

Property and Usage Rules

Another key factor in your decision is the way you intend to use the property. VA loans are strict about occupancy, while a conventional loan may offer more flexibility. The home must be your primary residence, especially if you want to qualify for a VA loan. You must move into the home within a reasonable time (usually 60 days) and intend to live there for most of the year. This means you cannot use this benefit to buy a rental property or a vacation home. You can buy a multi-unit property (up to four units), but you must live in one of the units as your primary home.

Conventional mortgages provide maximum versatility in this area. You can use conventional financing to buy a primary residence, a second home in the mountains, or a pure investment property to generate rental income. This makes them the preferred option for real estate investors or families looking for a getaway. If your goal is to build a real estate portfolio, you will likely need to use conventional financing after you have purchased your personal residence with a VA loan.

Frequently Asked Questions

What is the main difference between VA and conventional loans?

The main difference is who backs them; VA loans are backed by the government, whereas conventional loans are not. A VA loan is guaranteed by the Department of Veterans Affairs, permitting zero down payment and no PMI. Conventional financing is not government-backed, so it usually requires a down payment and PMI if you put less than 20% down. Still, it offers more flexibility for property types like second homes.

Is the VA funding fee worth it compared to paying PMI?

For most buyers, yes. The VA funding fee is a one-time cost that can be rolled into the loan. PMI is a recurring monthly expense that you pay until you have 20% equity. Over the first several years, the cumulative cost of PMI often exceeds the one-time funding fee, making this option more cost-effective, especially for those with little to put down.

Can I use a VA loan to buy a second home or vacation home?

No, you cannot use VA financing to buy a second home or vacation home. These loans are for owner-occupied primary residences only. If you want to buy a vacation home, you would need to use conventional financing or another type of mortgage, as VA loans are intended for primary residences.

Do I need a perfect credit score to get a VA loan?

No, you do not need a perfect credit score. The VA itself does not set a minimum, which allows for more flexibility in comparison to conventional loans. While most lenders look for a score of 620, they can be more flexible with these loans than with conventional options, especially if you have VA benefits and can show stable income and savings.

What happens to my VA loan if I move?

If you move, you have options. You can sell the home and pay off the loan, which restores your entitlement. You can also keep the home and rent it out, but you will use up part of your entitlement. You could also refinance the home into a conventional mortgage to turn it into a rental and free up your VA entitlement for a new purchase.

Making Your Final Choice

Ultimately, the decision boils down to your unique financial picture. If you are an eligible veteran or service member wanting to buy a home with no money down and lower monthly costs, a VA loan is an exceptional benefit. It provides a route to homeownership that is not available to the general public. The savings from avoiding PMI and securing a low interest rate can be substantial.

However, if you have significant savings for a down payment, excellent credit, and are looking at a second home or investment property, conventional financing might be your best bet. The flexibility it offers in property types and the ability to eventually cancel PMI are strong advantages. Speak with a few different lenders to get quotes for both options. Compare the interest rates, fees, and monthly payments, including PMI or the VA funding fee, to see which loan type leaves more money in your pocket over the long term.

Connect With Us

Please share – it really helps